© 2026 The Asclepius Initiative Inc. All Rights Reserved

Dual eligibility can feel complex, especially for individuals sorting through Medicare, Medicaid, and the different programs that connect them. People who qualify for both Medicare and Medicaid may have access to additional financial protections and benefits that help lower their health care costs. This page explains how dual eligibility works, outlines the different Medicare Savings Programs (MSPs), and reviews the coverage options available to those who qualify for both programs.

Medicare is the federal health care program for:

- People who are 65 or older

- Certain younger people with disabilities

- People with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a transplant, sometimes called ESRD)

Medicaid provides free or low-cost health care coverage to qualified people of all ages with low incomes, including children, pregnant women, older people, and people with disabilities.

With Medicaid expansion in Kentucky, it is available to adults aged 19-64 with incomes up to 138% of the Federal Poverty Level (FPL) and to pregnant women with incomes up to 200% FPL.

Some people may be “dual eligible.” This means they qualify for both Medicare and Medicaid. So, when a person meets criteria for both Traditional Medicare (Parts A and B) and Medicaid, they are considered “dually eligible.”

How Dual Eligibility Works

For those who are dual eligible, Medicare always acts as the primary insurance, while Medicaid steps in to fill the gaps, helping to pay for costs that Medicare doesn’t cover, such as premiums, deductibles, and co-insurance. Think of them as two puzzle pieces that work together to pay for your health care expenses.

Many dual-eligible individuals have multiple chronic conditions, behavioral health needs, and/or long-term services and support needs.

While all dual-eligible individuals have Medicare and some Medicaid benefits, their level of benefits may vary.

Dual-eligible beneficiaries (sometimes called “duals”) are enrolled in Medicare Parts A and/or B, and in Medicaid and/or in Medicare Savings Programs (MSPs). MSPs cover costs such as Parts A and/or B premiums and Parts A and B deductibles, coinsurance, and copayments, depending on the program. They may also help to cover prescription drug costs. While Medicare is administered by the federal government, Medicare Savings Programs are administered by the state; income qualifications can vary from state to state.

Medicare pays first when an individual is dually eligible and receives Medicare-covered services. Medicaid pays last, after Medicare and any other health insurance the individual has.

Similar to individuals who are not dual eligible, a person who qualifies for dual eligibility has the option of choosing Traditional Medicare or enrolling in a Medicare Advantage plan.

Full and Partial Dual Eligibility

There are two types of dual eligibility, full and partial. Both are administered through Medicare Savings Programs (MSPs).

Full dual eligibility means that the individual meets the criteria for Medicare, as well as the requirements for Medicaid in their state. This allows them to receive not only the benefits conferred by Medicare, but also benefits covered by Medicaid that may not/are not covered by Medicare, such as dental, vision, and long-term custodial care. The Medicaid benefits available to those who are fully dually eligible can vary from state to state. I’ll explain this a bit more in a minute, but those who have full dual eligibility fall into the MSP groups with the additional signifier of “plus.”

Partial dual eligibility means that the individual does not qualify for full Medicaid benefits, but, based on income and resources, may qualify under one of the other MSP resource categories. Depending on the Medicare Savings Program for which they qualify, Medicaid will pay for some or all of their Medicare Parts A and B premiums and cost-sharing. Because Partial-Benefit Dual Eligible Individuals do not qualify for full Medicaid benefits, they do not receive additional Medicaid-covered benefits, such as long-term services or supports.

Medicare Savings Programs (MSPs)

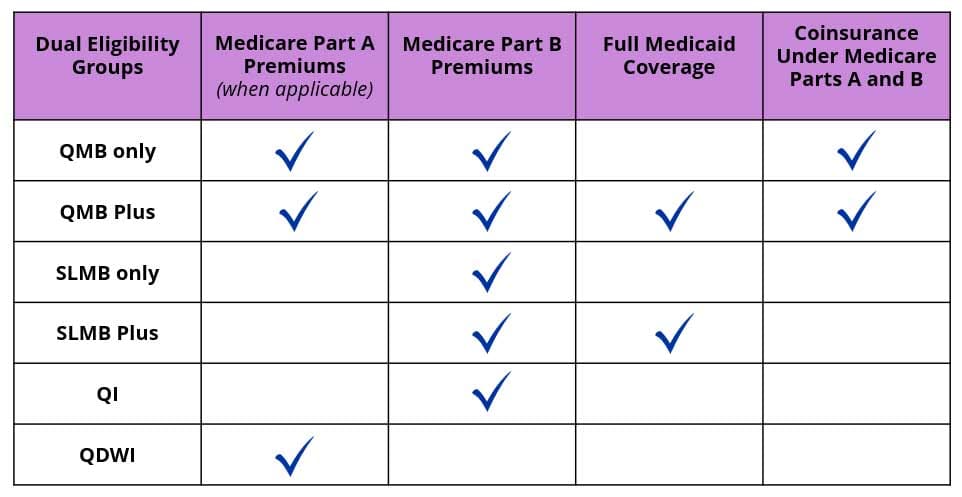

Qualified Medicare Beneficiaries are those with the fewest assets. The Qualified Medicare Beneficiary (QMB) program helps pay for Medicare Parts A and B premiums, deductibles, coinsurance, and copays, with eligibility set at 100% of the FPL. QMB is the most comprehensive MSP, covering all Medicare costs, including help with prescription costs.

The next level is called the Specified Low-Income Medicare Beneficiary (SLMB). This covers Medicare Part B premiums, with eligibility generally set between 100% and 120% of the FPL, and it also provides help with prescription drug costs. Neither this program nor the ones that follow cover copays, deductibles, or coinsurance costs.

The Qualifying Individual (QI) program, often called QI-1, helps pay Medicare Part B premiums for individuals with incomes above the Specified Low-Income Medicare Beneficiary (SLMB) level but below 135% of the FPL. However, states use limited federal funds for this program, so it’s limited to first-come, first-served. Those who seek QI assistance must reapply every year to remain in the program. Similar to QMB and SLMB, it helps with prescription drug costs.

Lastly, the Qualified Disabled and Working Individual (QDWI) program helps pay Medicare Part A premiums for people under age 65 with disabilities who lost their Social Security disability benefits and free Medicare Part A because they went back to work. To qualify, their income level must be below 200% of the FPL.

Income, Assets, and Eligibility

Income limits are based on a percentage of the FPL. The Centers for Medicare and Medicaid Services has officially updated the resource or asset limits for most MSPs. For QMB, SLMB, and QI programs, these have increased to $9,950 for individuals and $14,910 for couples in 2026. These represent the maximum “countable” assets, such as savings, stocks, and bonds, that a person can have to qualify.

This chart shows the benefits covered by Medicaid within the MSPs in table form, which is sometimes easier to understand.

Note that MSP plans which include the “plus” designation provide full Medicaid benefits.

Which plan a person qualifies for is primarily determined by income level and amount of assets.

There is also a classification known as “Other” duals. This group includes select cases, such as medically needy beneficiaries in a nursing home who are not eligible for prescription drug coverage or individuals in a state’s Pharmacy Plus demonstration.

Prescription Drug Coverage

Prescription drug coverage for dual-eligible individuals is primarily handled through Medicare Part D, but it is heavily subsidized by a program called Extra Help (also known as the Low-Income Subsidy or LIS).

If a person is dual eligible (full or partial), they automatically qualify for the Extra Help program. This means they do not have to pay a separate monthly premium for their drug plan, and the annual deductible is usually reduced to $0.

Even with Extra Help, an individual may still have a small “copayment” when they pick up their medicine. For 2026, the costs are capped at low rates.

Medicare Advantage and Special Plans

If someone chooses to join a Medicare Advantage Plan (and as a reminder, Medicare Advantage is Part C and is provided by private insurance companies approved by Medicare), there are special plans for dual eligibles. These plans typically include services covered by Medicare Parts A and B, as well as Part D, or drug coverage:

- Special Needs Plans or SNPs

- Medicare-Medicaid Plans (only available in certain states and not in Kentucky)

- Program of All-Inclusive Care for the Elderly (PACE) plans can help certain people who would otherwise need nursing home care get services that allows them to remain at home; PACE is free for those who are dual eligible; PACE is available in Kentucky

Click here for more information about these plan types.

A Special Needs Plan, or SNP (pronounced “snip”), is a specialized type of Medicare Advantage Plan (Part C). While standard Medicare Advantage plans are open to anyone with Medicare, SNPs limit their membership to people with specific diseases or characteristics to provide more tailored care.

Many dual-eligible individuals have access to SNPs and non-SNP options. A person can only join an SNP if they fall into one of these three specific categories: Dual Eligible or D-SNPs; Chronic Condition SNPs, or C-SNPs; and Institutional Special Needs SNPs or I-SNPs. To qualify for D-SNPs, a person must, at a minimum, meet the dual eligibility criteria.

Where to Get Help

For more information, contact the Kentucky State Health Insurance Assistance Program (SHIP). This free program provides information, counseling, and assistance to seniors and individuals with disabilities, their families, and caregivers. SHIP does not sell insurance; its only job is to help. Click here for their website or call 502-266-5571.

These and associated educational materials have been developed using our available resources. They are not intended to serve as advice or recommendations on selecting a specific type of coverage or plan. Any errors or omissions are unintentional.

These materials were supported by funds made available by the Kentucky Department for Public Health’s Office of Health Equity from the Centers for Disease Control and Prevention, National Center for STLT Public Health Infrastructure and Workforce, under RFA-OT21-2103.

The contents of these materials are those of the authors and do not necessarily represent the official position of or endorsement by the Kentucky Department for Public Health or the Centers for Disease Control and Prevention.