© 2026 The Asclepius Initiative Inc.

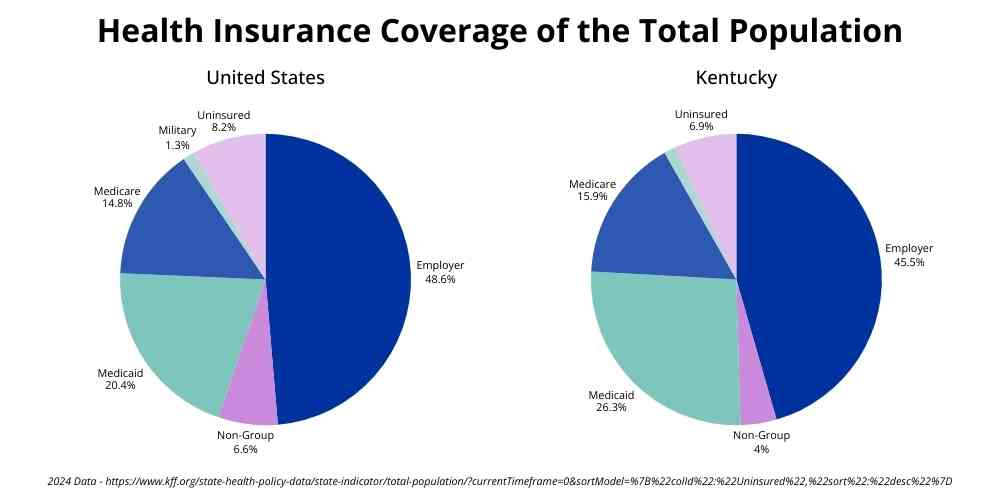

What is employer-sponsored coverage? The workplace is the most common source of health insurance in the United States. Nearly 49% of Americans, and more than 45% of Kentuckians, get their coverage through their work.

Employer-sponsored health insurance is exactly what it sounds like – health insurance offered through an employee’s workplace. Employers select the insurance carrier and plan option(s), and employees can decide whether or not to enroll.

While some employers pay the entire premium for their workers, the cost of the monthly premium is usually shared, with the employer typically paying at least 75% of the individual premium and the employee paying the balance through payroll deductions. KFF’s Employer Health Benefits Survey found that 2025 family premiums averaged $26,993, with workers paying an average of $6,850 and employers paying the rest.

For the employee, this arrangement can be cheaper than buying insurance through the Health Insurance Marketplace (kynect in Kentucky). Still, costs can vary, especially if Marketplace premium subsidies or cost-sharing reductions are available.

Who Typically Gets Employer-Sponsored Coverage?

Employer-sponsored coverage is most often offered as a benefit tied to full-time employment. Because of this, access to coverage depends not just on whether someone is employed, but also on the type of job they have, how many hours they work per week, and the size of their employer’s workforce.

In general, employer-sponsored coverage is more commonly available to people who work full-time, have been in their jobs longer, or work for larger companies that can afford to offer health benefits.

Not all jobs offer health insurance, even for full-time employees. KFF noted that 61% of employers with 10 or more workers offered health benefits in 2025, down from 68% in 2020. For employees of businesses that do offer coverage, the benefit may be available only to those who work a certain number of hours, or may provide only individual, not family, coverage. When health care coverage is not offered through work, people needing it must look for other options.

In these situations, individuals may be able to obtain coverage through the Marketplace, their spouse or partner’s plan, public programs such as Medicaid, Medicare, or the VA system, or other coverage options for which they may qualify.

What Are the Costs?

Employer-sponsored health insurance is not entirely “free” for the employee. The 2025 KFF survey found that, on average, workers paid 16% of the premium costs for individual coverage and 26% for family coverage.

Beyond monthly premiums, workers often pay out-of-pocket costs for:

- Deductibles

- Copays

- Coinsurance

Some employer plans have high deductibles, sometimes in the thousands of dollars. This means people may need to pay a large amount for non-preventive services before insurance begins to cover even some of the costs.

High out-of-pocket costs can make care harder to afford, even for people with insurance. Some people delay care or stretch their medications, such as taking them every other day instead of daily, because of cost.

Being aware of expected costs can help people budget for health care expenses and avoid surprises when they use their coverage to get care.

How Employer-Sponsored Coverage Decisions Are Made

When it comes to employer-sponsored coverage, both employers and employees make decisions. Employers decide which plans to offer and how much of the cost they will pay. They often try to balance the cost to the business with offering benefits that will help attract and keep workers.

Employees then decide whether to enroll in the coverage being offered and, if more than one plan is available, which option best meets their needs.

Employers decide:

- Whether to run their own health plan or use an insurance company

- If using an insurance company, which one to use

- How many plan options to offer

- What benefits are included

- What the deductible/copays/coinsurance/out-of-pocket maximum costs for the employee will be

- Will HSA/FSA/HRA accounts be offered; if so, how much will the company contribute

- Will the plan provide out-of-network benefits

- How much of the premium they will cover

Employees decide:

- Whether to enroll

- If allowed, whether to cover a spouse, partner, or dependents

- Which plan to select if multiple options are available

- Whether to enroll in an HSA, FSA, or HRA if available

Basically, employers decide what plans are offered, and employees choose from what is available.

Programs That Can Lower Health Care Costs

Some employers offer ways for employees to save money on health care costs. These accounts are connected to, but separate from, the health care plans.

In most cases, these programs are funded with pre-tax dollars. This means people can use money from their employer or their paycheck before taxes are taken out to help pay for certain medical expenses, which can lower overall costs.

Common types include:

- Health Savings Accounts (HSAs) – accounts that can be used with certain health plans to pay for qualified medical expenses; the employee, the employer, or both may fund these.

- Flexible Spending Accounts (FSAs) – accounts that allow people to set aside money during the year to pay for qualified medical expenses; the employee, the employer, or both may also fund these.

- Health Reimbursement Arrangements (HRAs) – employer-funded accounts that reimburse employees for qualified medical expenses, up to a set amount per year; unlike HSAs and FSAs, HRAs are not funded through payroll deductions; in some cases, HRA funds can also be used to pay premium costs.

These accounts can be used to pay “qualified medical expenses,” which are health care expenses the IRS says can be paid for with money in these accounts. Examples include deductibles, copays, and medications (prescription and over-the-counter), glasses, and contact lenses.

HSAs, FSAs, and HRAs have rules and contribution limits, and not all employers or insurance plans offer them.

Click here for a closer look at HSAs, FSAs, and HRAs.

What Happens When Employment Changes?

Since employer-sponsored health insurance is tied to employment, coverage is usually lost when employment changes (see COBRA information below for exceptions). This can leave people with little time to arrange new coverage.

Common situations that can affect continuity of coverage include:

- Job loss

- Reduced work hours

- Changing employers

- Divorce from or death of the policyholder

- Employer dropping coverage

- Turning 65

- Medicare must be the primary coverage for employees of organizations that employ fewer than 20 people

- Retirement

Options When Coverage Changes

When someone loses their job-based coverage or experiences a qualifying life event, they may be able to sign up for or modify coverage during a Special Enrollment Period. Special Enrollment Periods allow people to enroll in health care coverage outside the annual Open Enrollment window.

These Special Enrollment Periods are available for such events as:

- Losing job-based coverage

- Moving to a new area

- Getting married

- Having or adopting a child

- Changes in household income

After a qualifying life event, people usually have a limited time to sign up for or change coverage. The length of this window depends on the type of coverage and the situation.

Continuing Coverage through COBRA

In some cases, people may be able to keep their employer-sponsored coverage for a limited time through a federal law called COBRA. COBRA allows eligible individuals to continue the same health plan after leaving a job, but they must usually pay the full premium cost themselves.

For those who qualify, COBRA coverage must extend at least 18 months from the termination of employment, although it may be continued up to 36 months or longer under certain circumstances.

Why Understanding Employer-Sponsored Coverage Matters

Having employer-sponsored health insurance means more than just signing up for a plan. Knowing how coverage works and where limits or risks may exist empowers workers to make decisions that better meet their medical and financial needs.

Increased knowledge makes it easier to:

- Anticipate health care costs

- Ask questions about benefits and networks

- Anticipate how life changes may affect coverage and prepare for those coverage changes

- Avoid gaps in coverage

Clear, reliable information helps people to use their coverage more effectively, save money with HSAs, FSAs, and HRAs when available, and reduce uncertainty during times of change.

The Big Picture

Employer-sponsored coverage is how most working-age people in the United States get health insurance. Because it is so common, many families plan their jobs, finances, and health care around it. Over time, job-based coverage has become the default way people expect to stay insured.

But coverage tied to work does not always provide security. When employment changes, coverage costs can change too. In some cases, people lose access to care or struggle to afford it when they need it most.

These materials were supported by funds made available by the Kentucky Department for Public Health’s Office of Population Health from the Centers for Disease Control and Prevention, National Center for STLT Public Health Infrastructure and Workforce, under RFA-OT21-2103.

The contents of these materials are those of the authors and do not necessarily represent the official position of or endorsement by the Kentucky Department for Public Health or the Centers for Disease Control and Prevention.