For many people, health insurance is becoming harder to buy, harder to keep, and harder to use. The latest figures from KFF show that fewer people are signing up for Marketplace coverage in 2026, while many who do enroll are facing higher monthly costs, higher deductibles, and higher out-of-pocket expenses when they need care.

The Marketplace is how millions of people get health insurance when they do not have affordable coverage through a job, Medicare, Medicaid, or military benefits. In Kentucky, the Marketplace is known as kynect. With falling Marketplace enrollment and rising costs, it raises serious concerns about whether people can afford to stay insured and whether they can afford to use the coverage they have.

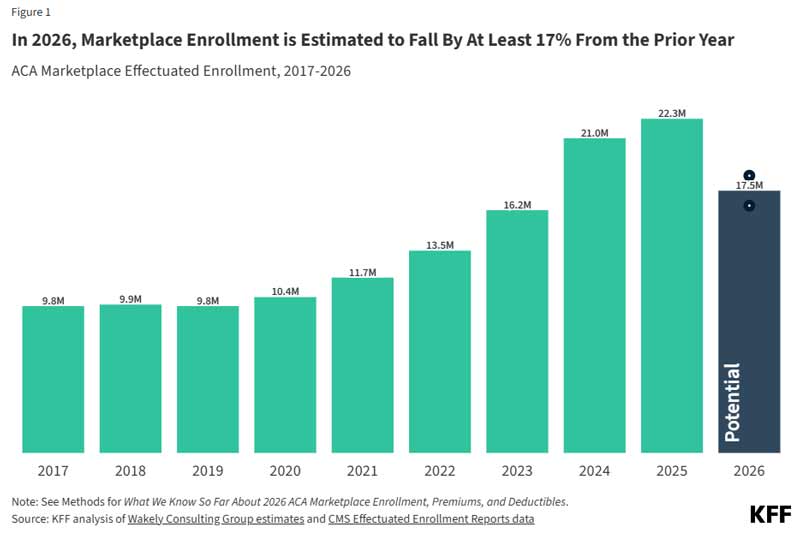

Fewer People Are Signing Up

The May 2026 KFF report shows that 23.1 million people selected Marketplace plans for 2026. That is one million people fewer than in 2025 and is the sharpest one-year drop in Marketplace plan selections since the ACA Marketplaces began.

Marketplace enrollment has fallen in 41 states, including Kentucky. KFF’s analysis shows just over 89,000 Kentuckians signed up for 2026 coverage through kynect, a 9% drop from last year.

Also, plan selections alone do not tell the whole story. A person can choose a plan during open enrollment, then lose coverage if the monthly premium is not paid. Based on projections from proprietary data from Wakely Consulting Group, KFF estimates that Marketplace enrollment could fall to about 17.5 million people in 2026, down from 22.3 million in 2025.

Enrollment Could Fall Even More

The latest KFF figures may be an early symptom of a growing problem. Marketplace enrollment is already down, and policy changes tied to H.R. 1, also known as the One Big Beautiful Bill Act, or OBBBA, are expected to cause more coverage losses in the years ahead.

The Congressional Budget Office estimates 16 million more people will be uninsured in 2034 than would otherwise be the case as a result of OBBBA, other ACA Marketplace changes, and the expiration of enhanced premium tax credits.

Beyond the widely talked-about Medicaid cuts, OBBBA also includes changes that may make it harder for people to get or keep Marketplace coverage. These include an open enrollment period that is 30 days shorter, more verification requirements, and new rules that require some people to verify eligibility before receiving premium tax credits or cost-sharing reductions. KFF notes that this pre-enrollment verification requirement would effectively end automatic renewals for many enrollees.

These changes matter because paperwork and shorter deadlines impose barriers to coverage. People may still qualify for subsidies or financial help, but lose coverage because the process of completing it on time becomes harder.

Costs Are Rising for People Who Stay Enrolled

One major reason enrollment is falling is that Marketplace coverage has become too expensive. Enhanced premium tax credits helped lower monthly premiums for many people who bought coverage through the Marketplace. Those enhanced tax credits expired at the end of 2025 and Congress failed to renew them.

Without that extra help, many people are paying considerably more each month. KFF found that average monthly premium payments increased from $113 in 2025 to $178 in 2026, a 58% increase.

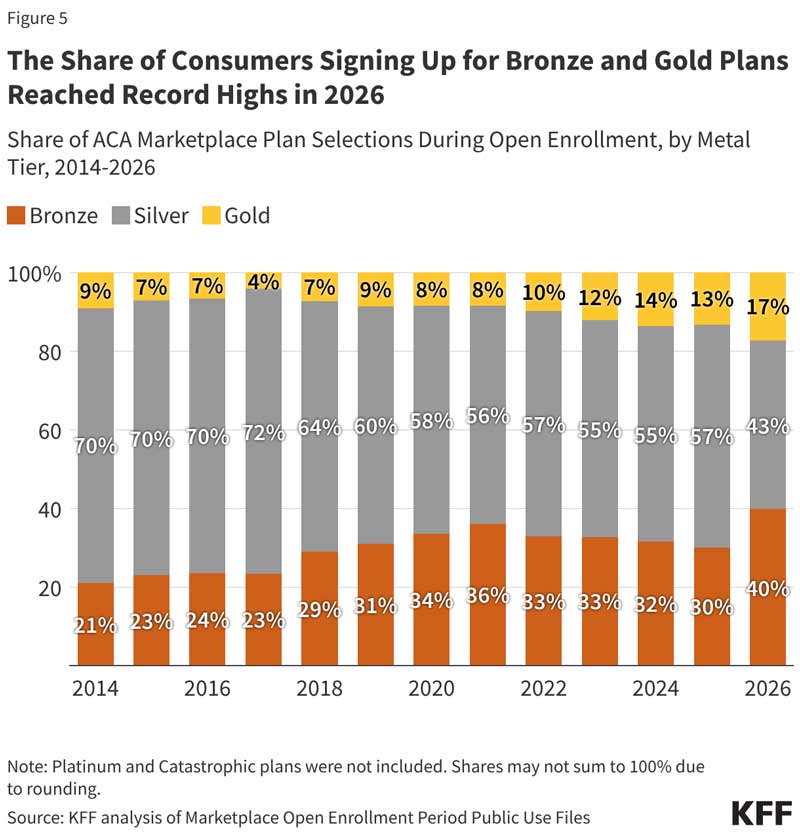

Some people are responding to higher monthly costs by choosing plans with lower premiums. KFF found that more Marketplace customers selected Bronze plans in 2026. Bronze plans usually have lower monthly premiums than Silver plans, but they often come with higher deductibles and out-of-pocket maximums, making it more difficult to pay for health services when care is needed.

In 2025, 30% of Marketplace customers selected Bronze plans. In 2026, that share jumped to 40%.

At the same time that premiums rose, the average Marketplace deductible increased by more than $1,000 per person, jumping from $2,759 to $3,786.

This creates a problem. A Bronze plan may be the only premium a person can afford each month, but if that person gets sick or injured, the higher deductible may make care too expensive to use.

Coverage Does Not Always Mean Care Is Affordable

The latest KFF findings show why health care affordability cannot be measured only by whether someone technically has health coverage. A person may be insured but unable to pay for care.

The Marketplace plays an important role in helping people get health insurance, especially when they do not have other affordable options. Yet, there are other factors at play. A higher premium, larger deductible, shorter enrollment period, or more paperwork can affect whether people stay covered and whether they can afford to use their coverage.

At The Asclepius Initiative, we believe everyone should have access to high-quality, affordable health care coverage from birth until death. Coverage should not depend on income limits, job status, annual enrollment rules, paperwork requirements, or whether a family can absorb another increase in health care costs.